In August 2018, a report on the state of cryptocurrency regulation across Africa came back with one obvious conclusion: most countries were undecided on what to do. Meanwhile, elsewhere in the world, a cryptocurrency bank, Kraken has been licensed, while some traditional banks are offering both cash and cryptocurrency accounts.

Indeed, in Ghana, till date, the Bank of Ghana has only said they were monitoring the emergence of cryptocurrency elsewhere on the continent and around the world, but there is not yet a policy on the subject.

In fact, 21 African countries had made no public stance on cryptocurrency regulation at the time, while only two had shared favorable stances about potential regulation. But, in what represents a major shift, Nigeria and South Africa—two of the continent’s largest economies—are stepping up regulatory plans.

But progress remains uneven across the continent. Kenya, which has typically been at forefront of adoption of financial technology solutions in Africa, has not set out concrete plans for regulation since its central bank warned local banks against cryptocurrency dealings.

“We seem to be in limbo,” says Aly-Khan Satchu, a Nairobi-based investor and financial analyst. “The spillover of the central bank governor taking such a strong stance against [cryptocurrency] remains the overarching situation.”

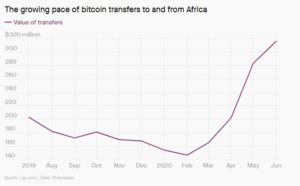

For their part however, local users and cryptocurrency startups across the continent are not exactly waiting for regulation to catch up. In fact, cryptocurrency trading has long taken off and is partly powered by homegrown exchanges which continue to operate in regulatory gray areas. For context, the total value of retail bitcoin transfers (worth less than $10,000 per transaction) in Africa reached $316 million as of June, according to research by Chainalysis, a blockchain market intelligence firm.

Full speed ahead

The growing volumes of transactions at local exchanges also suggest pace is unlikely to slow down. Luno, one of the continent’s oldest exchanges says monthly trading volume in Nigeria and South Africa alone topped $549 million in August—a 49% increase since the start of the year. (Luno also operates in Uganda and Zambia.) Meanwhile, BuyCoins, a three-year old Lagos-based exchange, says it has already processed $110 million in transactions so far this year, compared with $28 million for all of 2019.

There is also evidence of increasing adoption specifically due to the global Covid-19 pandemic as Luno reports a 122% increase in new customers across Africa between the fourth quarter of 2019 and the second quarter this year.

Among several operational challenges, Africans attempting to do business beyond the continent’s shores face risks of fluctuating exchange rates and difficulty around cross-border payments. And, amid further economic challenges posed by the Covid-19 pandemic, those underlying factors which hobble businesses have become more prominent, resulting in locals increasingly turning to cryptocurrency to facilitate international trade.

In addition to facilitating cross-border trade and payments, anecdotal data also suggests remittances are also a practical use-case for cryptocurrencies on the continent. It’s a scenario that’s plausible particularly given the historical context of the costs of sending remittances to Africa being higher than anywhere else. It’s a situation that likely drives African immigrants to “opt for cryptocurrency to try to maximize the value they can get,” Reitz explains.

“It is important that the space is regulated and properly guided by the financial authorities to ensure confidence and protection of the consumer,” says Stephany Zoo, head of marketing at Bitpesa, a Kenya-based exchange. “When you do that, it feeds back into the ecosystem and encourages innovation around this specific technology which there’s always been so much grey area around.”

The theme of regulation as a building block for fostering consumer confidence is a recurring one among cryptocurrency startup founders and insiders. By setting out requirements for cryptocurrency startups to operate, the belief is regulation will ultimately make it easier for interested customers to identify credible and licensed exchanges.

With fraudulent operators currently existing alongside credible cryptocurrency businesses without regulation, it leaves prominent startups and exchanges with the vital task of educating consumers to ensure more adoption and making cryptocurrencies more synonymous with safety than they are with scams.

But as is typical with regulation, there are potential pitfalls as recent history in some of Africa’s key tech markets show. For example, capital requirements for fintech startups in Nigeria are believed to pose barriers to entry. And in Lagos, Africa’s largest city, regulators ultimately banned motorcycle-hailing startups earlier this year after controversial attempts to regulate their operations. ”What we’d like to see is a phased approach,” Reitz says. “It can be very easy for regulators to want to regulate the entire industry from the onset but it could stifle innovation.”

As it turns out, the waiting game by Kenyan authorities may be coming at a cost of being at the forefront of the industry given the scale of local adoption: Kenya is the highest ranked African nation on the 2020 Global Crypto Adoption Index.

“The challenge stakeholders will be concerned about is that the advantage is being eroded the longer Kenya does not take an appropriate stance towards this market,” Satchu tells Quartz Africa. “This is fertile ground to look to develop a leading edge cryptocurrency market on the continent—the question is if the regulators want that.”

")

{kind=link}