Days a go, MobileMoney Limited (MML), the digital finance sister company of MTN Ghana issued an SMS circular informing its over 13 million customers that beginning July 1, 2023, the maximum threshold for cash out transaction fees will be increased 100% from the current GHS10 to GHS20.

Per the circular, all cash out transactions of up to GHS2,000 will attract 1% fee, which means the highest fee is now GHS20; beyond which it will remain fixed. Hitherto, the 1% fee was applied to amounts only up to GHS1,000, and it came to a maximum of GHS10.

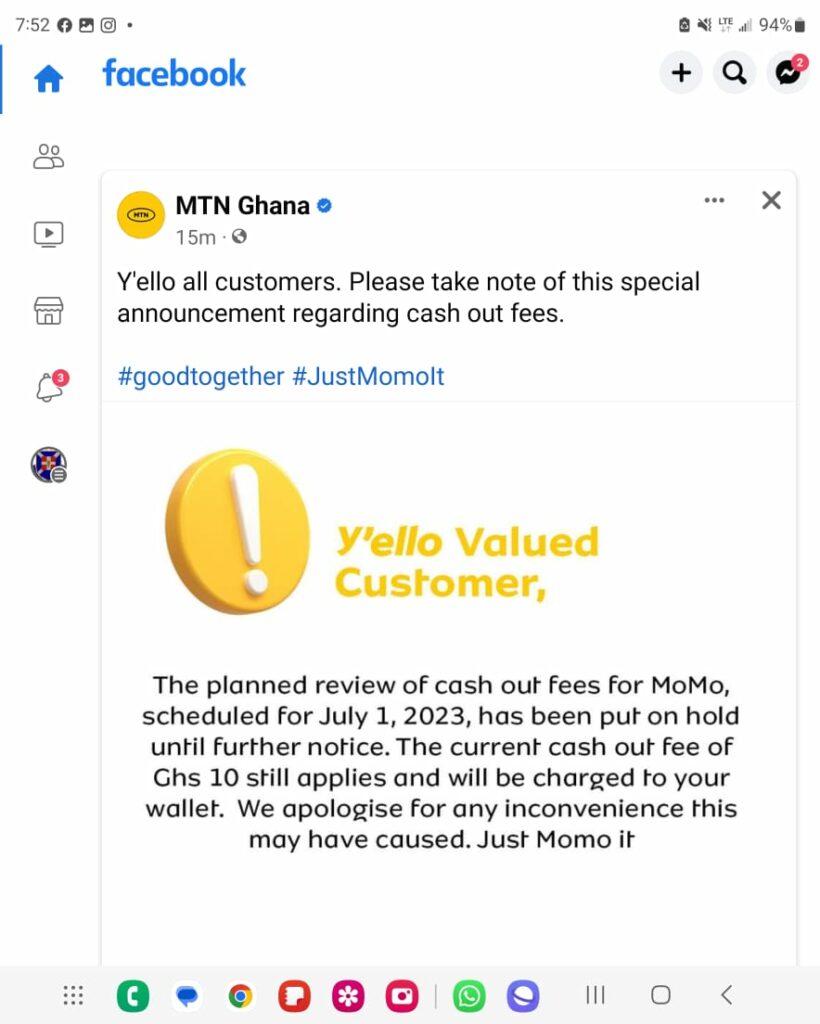

Here is exactly what the circular said:

Before we move forward, let me state categorically, for the avoidance of doubt, that this decision of MobileMoney Limited (MML) HAS ABSOLUTELY NOTHING TO DO WITH THE SIGNIFICANT MARKET POWER (SMP) DECLARATION ON MTN GHANA. Take note that MTN’s SMP status only applies to MTN Ghana (the telecoms wing) and NOT MobileMoney Limited (the mobile money wing). MTN Ghana is regulated by the National Communications Authority (NCA) and MobileMoney Limited is regulated by the Bank of Ghana (BoG). The BoG has NOT named MobileMoney Limited as SMP.

So, this decision to burden Ghanaians with higher cash out fees is entirely on MTN Mobile Money and nothing to do with regulatory direction or any thing of a sort. In fact, we have checked with the BoG to find out if MTN even had approval for the increment and what the regulatory guidelines are on that. We are yet to get some answers.

While we were waiting for official response from BoG, MTN made an announcement on their official Facebook page that the planned increment has been put on hold until further notice.

Take note that the suspension is until further notice and not indefinitely. The last time MTN suspended a planned price hike of data bundles until further notice, it went back later and actually increased the price. It is expected that in this case, the regulator will intervene and provide its guidance away from prices increases.

As we wait for how this whole thing will pan out, let’s take a look at the actual factors and other possible reasons why MTN has had to arrive at this rather unpopular decision.

As was to be expected, there have been widespread public outcry against the out-of-sync decision by MTN, with some even threatening to abandon their MTN mobile money wallets and go for others. I wonder whether that would be a good thing for anyone to do now, but that is what some people have said.

The other question people are asking is simply WHY MTN?

- Why burden Ghanaians with higher mobile money transaction fees now that times are this hard for the average Ghanaian living in this harsh and bankrupt economy, plagued with skyrocketing inflation, ever-increasing prices of goods and services, low income and rampant job losses?

- Why do this to your loyal customers, as the biggest market player with over 13 million mobile money customers, making all the money in that space?

- Why this at a time when it is generally expected that service fees will rather go down as more and more Ghanaians adopt and use digital finance?

- Is this part of MTN’s subtle propaganda moves in response to government policies that it is not happy about?

We have asked MTN for some explanations. But as we wait for their official response, this is what has emerged:

MoMo Agents

Mobile Money agents in the country have come out and confessed to being the masterminds behind the planned increase in cash out transaction fees.

Executive Secretary of the Mobile Money Agents Association of Ghana (MMAAG), Evans Otumfuo, who is the spokesperson for the agents, said in an interview that since the inception of mobile money by MTN in 2009 till date, service fees have not been reviewed. As a result, the commissions paid to agents have also not been reviewed.

According to him, this is happening in the face of ever-increasing operational cost, plus the fact that the earnings of agents have also reduced drastically because thousands of Ghanaians have entered the space and the competition has become even tighter. Now MTN alone is reporting about 400,000 merchants and agents across the country.

It would be recalled that in April this years, all the major mobile money agents associations in the country, came together and made a presentation to MTN with their grievances, demanding for increases in commissions, transparency in fees reconciliation, and prompt payment of commissions among other things. They even threatened to go on strike on May 10, if nothing was done about their complaints.

Some of the agents have on their own been trying to cut their losses by compelling customers to cash out bigger amounts in batches of GHS1,000 at a time, so that they (the agents) can charge the maximum GHS10 on every GHS1,000 and make some money.

So, clearly, the need to increase agents’ commissions is the main driving force behind the MTN’s decision to burden customers with a hike in cash out transaction fees. Moreover, since 2009, when MTN first introduced mobile money in the country, service fees has never been adjusted in spite of the fact that inflation, cost of operations and general overheads for MTN itself have increased greatly. Indeed, MTN in particular, also made huge sacrifices investing in mobile money and running at a loss for a good six years before things started turning around for them. So, maybe the price review must happen at time point, but is this a good time?

E-Levy

Beside the actual stated reason for the planned increase, there may be other factors and reasons why a company like MTN would consider an increase in one of the fee elements as a good move. When the obnoxious 1.5% electronic transfer levy (e-levy) was introduced by the government in 2021, mobile money operators like Vodafone and GhanaPay zero-rated transfer fees to all networks, while MTN reduced the fees for on-net P2P transfers from to 1% to 0.75%. So, the maximum fees for transfers dropped from GHS10 to GHS7.50.

Quite a number of industry watchers thought that because MTN makes, by far, the biggest revenue in the mobile money space, it was going to be the one to zero-rate transfer fees. But it would appear that, that is where they make a greater chunk of their mobile money revenue, so it was not going to be sustainable to just zero-rate that. So they opted for a 0.25% reduction instead.

However, due to the obnoxious e-levy, lots of Ghanaians either abandoned money transfers, adopted other legitimate ways of getting moneys transferred on their behalf without paying e-levy, or reduced the amounts they transferred in a day to GHS100 for wallets, and GHS20,000 for bank accounts just to avoid e-levy. As a result, MTN, like the other mobile money players, suffered a double loss – they had reduced service fees to cushion Ghanaians in the face of e-levy, but Ghanaians also cut down on the extent to which they do money transfers and resorted more to cash out transactions.

The situation affected MTN’s revenue from mobile money in 2022. Let’s look at MTN’s mobile money revenue growth trends between 2019 and 2022:

As indicated above, between 2019 and 2020, the growth was almost GHS300 million. Then in the following year its shot up to almost GHS500 million. But per the 2022 report, mobile money revenue hit 1.9 billion, which means growth was less than a GHS200 million. Again, mobile money’s contribution to the company’s overall service revenue also declined from 22.5% to 19.6% year-on-year.

So, it would appear that this new decision to increase cash out transaction fees from a maximum of GHS10 to GHS20 is a two-edged sword; to make some money to shore up revenue from the sector, and also to discourage customers from doing cash out and revert to transfers as the country goes digital. This is particularly so, as e-levy has been reduced to 1% and the industry has reported seeing some improvements in transfers since.

SMP

Whereas MTN Ghana’s SMP status has completely nothing to do with its Mobile Money sister company, some of the effects of regulatory interventions in respect of the SMP status is denying MTN of revenue, so they may have been compelled to increase cash out transaction fees to meet the extra cost of reviewing agents’ commissions upwards, instead of just taking money from another revenue line to meet that cost.

For instance, because MTN is the SMP, the interconnect fees supposed to be paid to it by other telcos who terminate calls on MTN, have been reduced by 30%. As a result of that, MTN was denied some GHS86.6 million between October 2020 and December 2022. That is moneys they could have fallen on to increase mobile money commissions if it was available.

Secondly, MTN was stopped from keeping its very affordable Dara Zone bundles on the market and that has most likely discouraged the loads of students who used to patronize it for their school work from buying it at the new and more expensive prices. The intent of the regulator for ordering MTN to review the prices of that package upwards is to ensure that MTN does not have the lowest prices on the market.

In fact, MTN has been directed by NCA not to have the lowest tariffs of voice, SMS and data on the market. All that is designed to make MTN’s competitors be able to compete on pricings. So while some of MTN’s interconnect fees have been left for the other telcos to keep, they are also being allowed to offer lower prices than MTN to possibly deny MTN more revenue.

All of this could be reasons fuelling the efforts to find other ways to increase its revenue and be able to meet its operational cost, hence the decision to use the merchants and agents’ demand as a primary reason to increase cash out transaction fees. Indeed, MTN may also be using that move as a protest to the policies being implemented to constrain its operations.

NCA claims the declaration of MTN as an SMP is not meant to stifle its operations. But the manifestations of the regulatory interventions have done nothing but place constraints on MTN, even though the company seem to always find a way to continue growing in spite of those constraints.

Financial Inclusion

Having said all that, let me make the point that it is true MTN made huge loses in the first six years of rolling out mobile money. It is true that a lot of the losses was because agents, at the time, had easy access to customers’ secret PINs and therefore could easily steal their money and leave MTN with debts to settle. It is true that e-levy has affected mobile money earnings for MTN and all other players in the industry. It is true that SMP constraints are denying MTN revenue. But I don’t see how MTN MobileMoney would think service fee increase is the way to go at a time when financial inclusion is the watch word in the industry and affordability is the main driving force for inclusiveness.

It is my hope, therefore, that as MTN has suspended the planned increase, it will find another innovative way to satisfy its merchants outside of increasing service fees. Any strategy that depends on increasing service fees at this time, threatens to derail the gains made in inclusion and probably discourage further adoption and usage of digital finance.

{kind=link}